Incorporation Policies

These policies augment the Governor’s Office of Planning and Research (OPR) “Guide to the LAFCO Process for Incorporations”. Where these local policies differ from the OPR Guidelines the local policies shall apply. These policies are not intended to preempt state law. Should these policies conflict with the provisions of law, the provisions of the CKH Act and related statutes shall prevail. Unless otherwise specified herein, proposals for incorporation are subject to all policies and requirements that apply to proposals and applications submitted to Santa Clara LAFCO.

1. CERTIFICATE OF FILING AND TIME LIMITATIONS

- In order to deem the incorporation application filed, issue the Certificate of Filing and set a hearing date for the proposal, all application requirements must be completed (§56651). The Certificate of Filing will not be issued by the Executive Officer until all of the filing requirements have been met including the comprehensive fiscal analysis and information sufficient to facilitate an environmental determination pursuant to CEQA.

- To ensure that the petition signatures remain sufficient and that the proposal remains current, the application requirements must be completed within 24 months following the date of the Certificate of Sufficiency or the date of adoption of the resolution making the application.

- If the application remains incomplete after 22 months, LAFCO staff will notify the proponents at least 60 days before the 24‐month deadline. The Commission may allow an extension of the 24‐month time period, on a case by case basis.

- LAFCO staff will use its best efforts to ensure timely completion of each procedural requirement in the incorporation process, including, but not limited to, preparing requests for financial information as early as possible following the close of the fiscal year; giving appropriate notice; initiating agency consultations; and convening meetings related to revenue transfers.

2. INCORPORATION PROCESSING FEES

- The actual costs for processing the incorporation application are the proponent’s responsibility. Application costs include consultant costs for preparing the comprehensive fiscal analysis and the environmental review documents, LAFCO staff time, legal counsel costs and other related expenses incurred by LAFCO in the incorporation proceedings.

- Incorporation proposals are charged on an actual cost basis with a deposit required when the proposal is initiated. The cost of the proceedings will be much higher than the initial deposit. The deposit allows staff to open a file and initiate the determination of petition sufficiency and begin meetings with the proponents to develop a time frame and cost estimates.

- Consultants will be hired for the preparation of the comprehensive fiscal analysis and CEQA analysis / documents. Each consultant’s total cost will be divided into costs for each sub task. Prior to commencement of each sub task, the proponents must make a deposit in the amount of the estimated cost for that task. LAFCO will not authorize the consultant to commence work on the task until the funds are received. At the end of each task a final accounting will be done. Any amounts due must be paid within 30 days. Any refunds will be applied to the subsequent task or refunded. The actual amounts of the deposits will be determined after the consultant contracts are negotiated.

- LAFCO staff will provide the proponents an initial estimate of the costs of the incorporation proceedings. The terms of payment will be stated in an agreement to be executed between LAFCO and the proponents.

3. INCORPORATION BOUNDARIES

- The Commission will review proposal boundaries, as submitted by proponents. Alternatives to the proposal must also be considered by LAFCO. The Executive Officer will convene a meeting to identify logical boundary alternatives for the new city at the earliest date possible. The meeting will include the proponents.

- The Commission may modify proposed boundaries and order the inclusion or deletion of territory to accomplish its goal of creating orderly boundaries.

- A proposed incorporation must satisfy a demonstrated need for services, and promote the health, safety, and welfare of the community.

- A proposed incorporation or formation must not conflict with the normal and logical expansion of adjacent governmental agencies.

- An area proposed for incorporation must be compact and contiguous, and possess a community identity.

- The proposal boundaries and alternatives shall not create islands or areas that would be difficult to serve.

- Areas included within the proposed incorporation boundaries should consist of existing developed areas and lands, which are planned for development.

- Inclusion of agricultural and open space lands within the boundaries of a proposed city is discouraged.

- Incorporation boundaries should be drawn so that community based special districts are wholly included within or excluded from the incorporation area, unless the Commission determines that there is either an overriding benefit to dividing the district or that there is no negative impact from dividing the district.

4. SERVICES TO INCORPORATION AREA

- Applicants must demonstrate to LAFCO that the proposed city will have the ability to provide adequate facilities and services in the incorporation area, at no less than the level of services provided in the area prior to incorporation.

- New cities should assume jurisdiction over as many services in the incorporation area as are feasible.

5. SPECIAL DISTRICTS AFFECTED BY INCORPORATION PROPOSAL

- District territory included in an incorporation area should be detached from the district or the district dissolved unless LAFCO determines that there is an overriding reason to retain the district.

- Detachment of territory from a region‐wide special district which provides service to multiple communities outside the incorporation area is discouraged, unless the Commission determines that there is an overriding reason for the detachment.

6. TIMING AND INITIATION OF NEW CITY’S SPHERE OF INFLUENCE

- The Commission may determine the sphere of influence for the new city at the time the incorporation is approved or no later than one year from the effective date of incorporation. The new city may initiate a Sphere of Influence application. In the absence of an application within the time frame necessary for sphere adoption, the Commission will adopt an initial Sphere of Influence boundary for the city which will be coterminous with the city’s boundaries.

7. ENVIRONMENTAL REVIEW OF INCORPORATION PROPOSALS – CEQA

- LAFCO is the Lead Agency for incorporation proposals.

- The Executive Officer is the Environmental Coordinator for LAFCO, and is responsible for the environmental review process.

- The Environmental Coordinator will prepare the Project Description.

- The Project Description will include the proposal as submitted. The Project Description may identify alternatives being considered for the project and a sphere of influence boundary for the proposed city.

- Under the direction and management of the Environmental Coordinator, the environmental review will be initiated as early as feasible and will be completed as cost‐effectively as possible.

8. COMPREHENSIVE FISCAL ANALYSIS AND REVENUE NEUTRALITY NEGOTIATION PROCESS

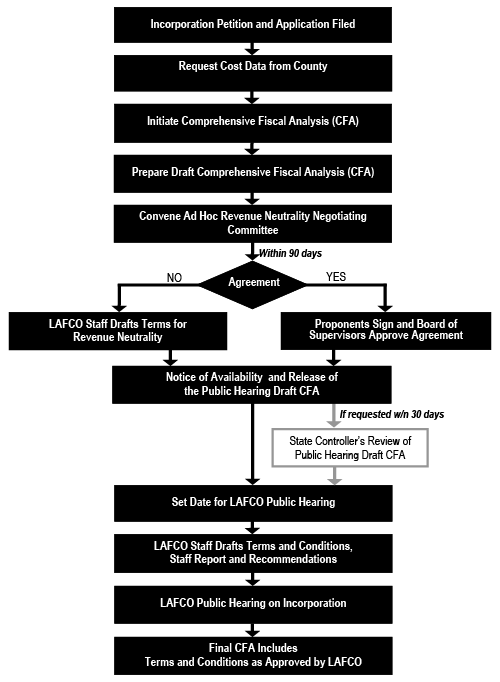

The general process for preparing the comprehensive fiscal analysis and negotiating the revenue neutrality is outlined in the following flow chart .

8.1 Initiate Comprehensive Fiscal Analysis

- LAFCO will retain a financial consultant qualified to prepare the Comprehensive Fiscal Analysis (CFA) and related documents necessary for the project, consistent with LAFCO’s usual and customary contract procedures.

- The fiscal analysis will evaluate the proposal as submitted as well as the identified alternatives.

- A detailed timeline for the CFA process will be developed by LAFCO in consultation with the consultants hired to prepare the CFA.

- The Draft CFA will be prepared as early as possible to support revenue neutrality discussions.

8.2 Ad Hoc Revenue Neutrality Negotiating Committee

- The LAFCO Executive Officer will convene an ad hoc revenue neutrality negotiating committee to develop a revenue neutrality agreement as soon as possible after the draft CFA information becomes available.

- Members of the ad hoc revenue neutrality negotiating committee shall include representatives of the County and representatives of the incorporation proponents and other affected agencies, as needed.

- At the commencement of the negotiations or earlier, each party will provide a list of its representatives and designate one principal representative. Additional members may be added after negotiations commence with the agreement of both parties.

- LAFCO staff will attend meetings of this committee in order to facilitate discussion, provide technical assistance and ensure compliance with LAFCO policies. LAFCO staff has the discretion to request attendance by its consultants.

8.3 Timing and Adoption of Revenue Neutrality Agreement

- The Draft CFA is a prerequisite to revenue neutrality negotiations.

- The ad hoc revenue neutrality negotiating committee will have up to 90 days to negotiate a revenue neutrality agreement. The 90 days commences from the first meeting of the ad hoc committee following the release of the Draft CFA.

- Within the 90 day period, if the parties reach agreement, they shall provide a written revenue neutrality agreement to the Executive Officer; the agreement will be signed by proponents. County representatives to the committee will place the agreement on the County Board of Supervisors agenda within the 90 day period.

- The terms of the Revenue Neutrality Agreement will be included in the budget projections and feasibility analysis in the Public Hearing Draft CFA.

- If agreement does not occur within the 90‐day negotiating period, LAFCO staff will draft proposed terms and conditions for use in the Public Hearing Draft Comprehensive Fiscal Analysis and for recommendation to the Commission at its public hearing.

- The revenue neutrality committee may reduce the time period for reaching agreement with the consent of all parties.

8.4 Public Hearing Draft CFA

- A Notice of Availability will be prepared by LAFCO staff and the Public Hearing Draft CFA will be circulated and made available to the public no less than 30 days prior to LAFCO’s hearing on the proposal. The Public Hearing Draft CFA includes terms of the revenue neutrality agreement, if agreement has been reached or terms to be determined by LAFCO if agreement has not been reached.

8.5 State Controller Review of Comprehensive Fiscal Analysis, if Requested

- Any party may request review of the Public Hearing Draft Comprehensive Fiscal Analysis within 30 days of the release of the Notice of Availability of the Public Hearing Draft CFA. The written request shall be made to the LAFCO Executive Officer and should identify the specific elements that the State Controller is being requested to review and state the reasons for review of each of the elements.

- The requestor is responsible for all costs related to the request, and shall sign an agreement to pay such costs.

- The requestor shall deposit a fee in the amount of the total estimated cost of the review at the time the request for review is filed. The deposit will include the estimated charge by the State Controller, LAFCO staff costs, and costs for any consultants required to assist the State Controller with the review. The difference between the actual cost and the estimate shall be refunded / charged to the party initiating the request after the review is complete.

8.6 Final CFA

- The Final CFA will include the terms and conditions approved by LAFCO and will be prepared following the Commission’s determinations and approval of the incorporation.

9. FINANCIAL ASSUMPTIONS AND FISCAL ANALYSIS REQUIREMENTS

- All assumptions and calculation methodologies used for the fiscal calculations shall be clearly identified and detailed in the CFA.

- The CFA shall calculate the proposed city base year costs consistent with the OPR Guidelines (Section V. 3.)

- The base year or “prior fiscal year” shall be the basis of financial calculations and determinations, as defined in Government Code 56810(g) as follows: “the most recent fiscal year for which data on actual direct and indirect costs and revenues needed to perform calculations required by this section are available preceding the issuance of the certificate of filing”.

- Costs of services in the proposal area shall be based on existing levels of service provided in the proposal area by the County and other agencies during the “base year”.

- When proposed city functions and services have not previously been provided by an agency prior to incorporation (e.g. new city general administration costs that are not transferred from another agency), the cost projection basis for the proposed city’s future expenditures for those services and functions shall be based on cities with similar population and geographic size that provide similar level and range of services.

- Revenue projections for anticipated future city revenues will be “conservative”; where the revenue projection is estimated as a range, the lowest number in the range will be used for calculating future city budgets.

- Property tax projection calculations for projecting the future city revenues will include the rate of increase in the assessed value (not greater than 2% annually). Property tax revenue projections based on market driven property tax reassessments (e.g. increases in home re‐sale values) should not be relied upon for calculating future year city budgets and determining feasibility.

- The CFA shall include the proposed city budget, projected for a minimum of ten years in order to 1) evaluate long term feasibility, 2) consider the effects of the new city’s repayment to the County for its first year services and 3) project the effects of foreseeable shifts in state subventions, etc.

- The CFA should include an annual appropriation in the new city budget for contingencies of 10% in each budget year evaluated. The CFA should include an additional reserve of 10% in any given year in the new city’s budget projection.

- The CFA will calculate the estimated property tax transfer and the total net agencies’ cost of providing service in the proposed incorporation area. The Commission makes the final determination of costs and the transfer of property taxes.

- Financial feasibility shall be based on the ability of the new city to maintain pre‐incorporation service levels.

- The CFA will include revenue sources that are currently available to all general law cities. Projections will not be based on potential revenue sources not currently applicable in the area or new revenues which might become available through the discretionary actions of a future city council.

10. BASIS AND ASSUMPTIONS FOR REVENUE NEUTRALITY

Revenue neutrality intends that any proposal that includes an incorporation should result in a similar exchange of both revenue and responsibility for service delivery among the county, the proposed city, and other subject agencies. It is the further intent of the Legislature that an incorporation should not occur primarily for financial reasons (§56815). Pursuant to Government Code §56815 LAFCO will make findings and/or impose conditions/mitigations to equalize the transfers of revenue and service.

- The revenue neutrality agreement or any proposal for LAFCO terms and conditions for revenue neutrality shall include:

- A criteria and a process for modification by the affected agency and the city after incorporation

- A description of methodologies and assumptions leading up to the terms of the agreement

- Identifiable and recurring revenues and expenditures only

- The revenue neutrality agreement or any proposal for LAFCO terms and conditions for revenue neutrality shall exclude:

- Anticipated or projected revenue growth or sources of revenue dependent on discretionary actions by a future city council

- Services funded on a cost recovery basis (such as permits/building inspection) which are, by definition, revenue neutral

- Costs of capital improvements

- The following additional policies apply to the revenue neutrality agreement or any proposal for LAFCO terms and conditions for revenue neutrality:

- Fiscal impacts to restricted and unrestricted revenues should be evaluated separately. A city may pay a portion of its annual revenue neutrality payment with restricted funds if both agencies agree, and if a legal exchange mechanism can be created to do so.

- Fees charged by the county for services to other jurisdictions (such as property tax administration fees or jail booking fees) should be included as an off‐setting county revenue in the calculation of fiscal effects on the county.

- Countywide costs of regional services and general government, including the County Administration, Clerk of the Board, AuditorController and other administrative government functions which are required to support county governance of both incorporated and unincorporated areas should not be included in defining services or revenues transferred to the new city.

11. EFFECTIVE DATE OF INCORPORATION

- The effective date of incorporation should be considered in revenue neutrality negotiations. LAFCO will establish the effective date. The effective date should be set to allow adequate initial account balances for the new city as it assumes service responsibilities, but should not otherwise conflict with the intent of fiscal neutrality or exacerbate County revenue losses.